Helpful real estate information and tips

Ways Your Home Equity Can Help You Reach Your Goals

If you’ve owned your house for at least a couple of years, there’s something you’re going to want to know more about – and that’s home equity. If you’re not familiar with that term, Freddie Mac defines it like this:

“. . . your home’s equity is the difference between how much your home is worth and how much you owe on your mortgage.”

That means your equity grows as you pay down your home loan over time and as home values climb. While it’s true home prices dipped slightly last year, they rebounded and have been climbing in many areas since then. Here’s why that price growth is good news for you.

In the latest Equity Insights Report, Selma Hepp, Chief Economist at CoreLogic, explains:

“With price gains continuing to help homeowners build wealth, equity has reached a new high and regained losses that resulted from declines last year. And while the average U.S. homeowner gained over $20,000 in additional equity compared with the third quarter of 2022, some markets are seeing larger increases as price growth catches up.”

And that figure is just for the last year. To help you really understand how that number can add up over time, the report also says the average homeowner with a mortgage has more than $300,000 in equity. That much equity can have a big impact.

Here are a few examples of how you can put your home equity to work for you.

1. Buy a Home That Fits Your Needs

If your current space no longer meets your needs, it might be time to think about moving to a bigger home. And if you’ve got too much space, downsizing to a smaller one could be just right. Either way, you can put your equity toward a down payment on something that fits your changing lifestyle.

2. Reinvest in Your Current Home

And, if you’re not ready to move just yet, you can use the equity you have to improve your current home. But it’s important to consider the long-term benefits certain upgrades can bring to your home’s value. A real estate agent is a great resource on which projects to prioritize to get the greatest return on your investment when you sell later on.

3. Pursue Personal Ambitions

Home equity can also serve as a catalyst for realizing your life-long dreams. That could mean investing in a new business venture, retirement, or funding an education. While you shouldn’t use your equity for unnecessary spending, using it responsibly for something meaningful and impactful can really make a difference in your life.

4. Understand Your Options to Avoid Foreclosure

While the number of foreclosure filings remains below the norm, there are still some homeowners who go into foreclosure each year. If you’re in a tough spot financially, having a clear understanding of your options can help. Equity can act as a cushion if you’re not able to make your mortgage payments on time.

Bottom Line

If you want to know how much equity you have in your home, let’s connect. That way you have someone who can do a professional equity assessment report on how much you’ve built up over time. Then let’s talk through how you can use it to help you reach your goals.

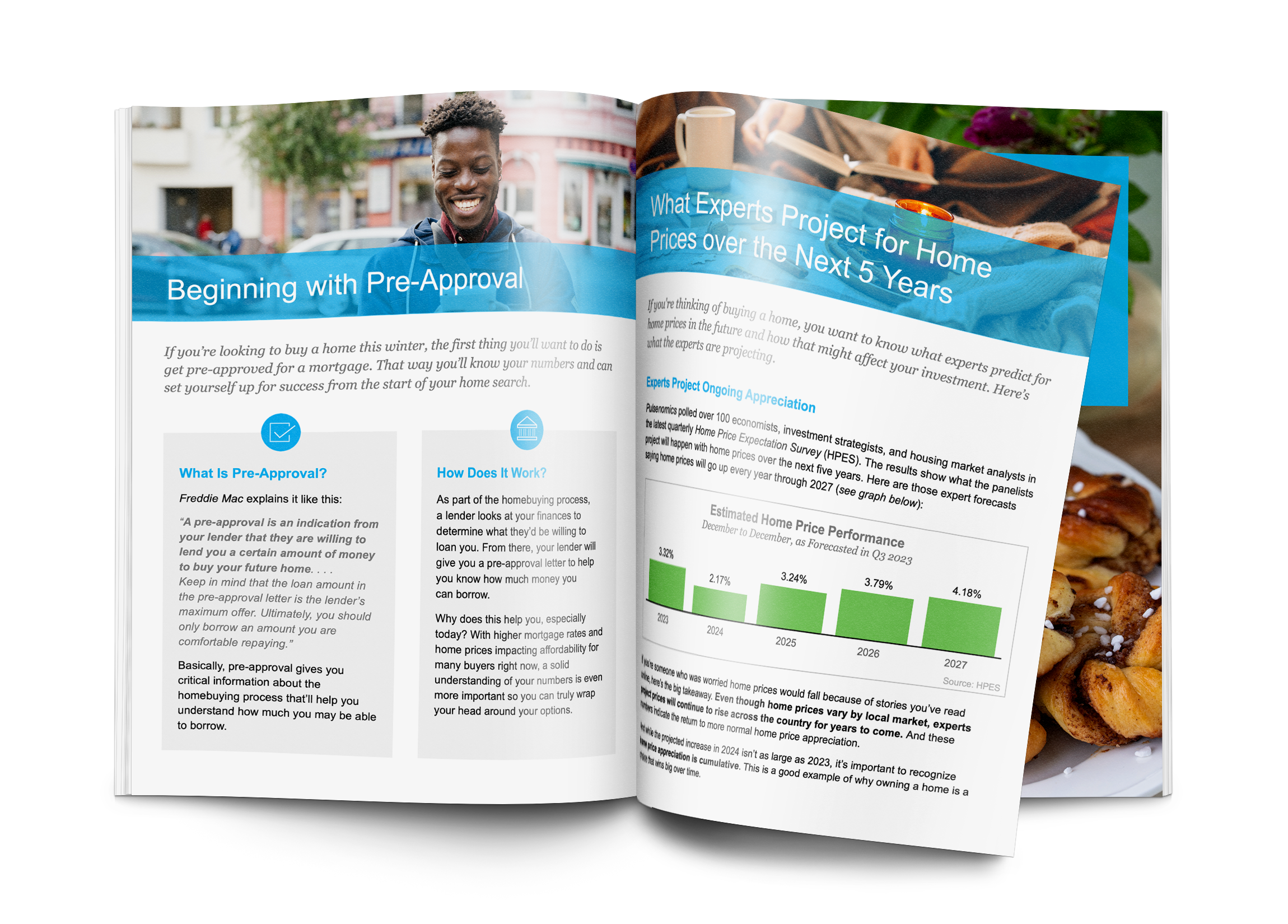

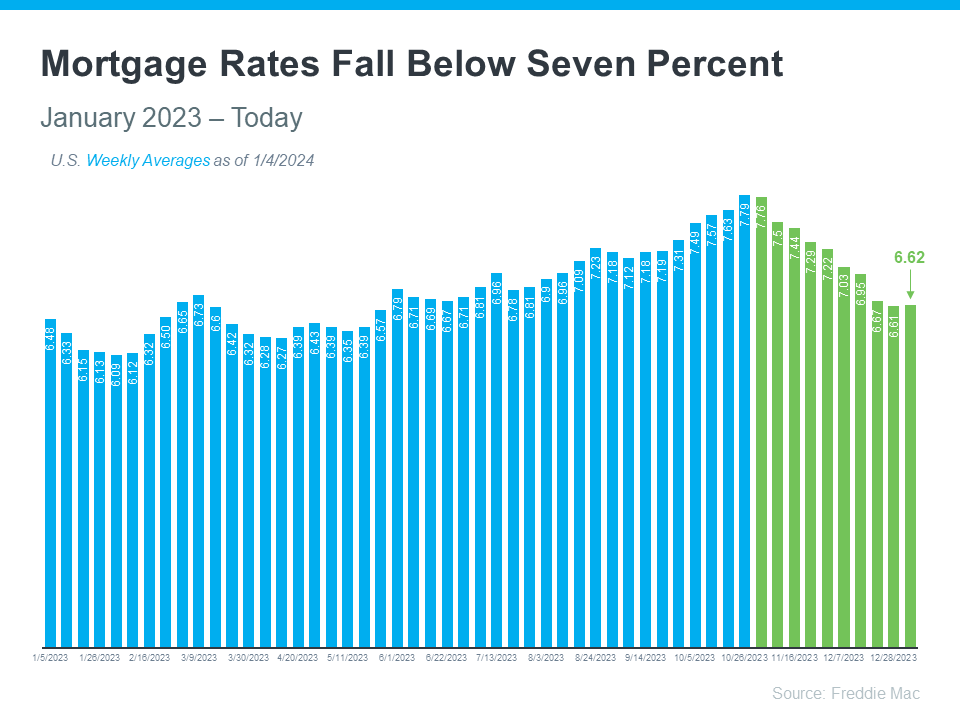

What Lower Mortgage Rates Mean for Your Purchasing Power

If you want to buy a home, it's important to know how mortgage rates impact what you can afford and how much you’ll pay each month. Fortunately, rates for 30-year fixed mortgages have come down significantly since the end of October and are currently under 7%, according to Freddie Mac (see graph below):

This recent trend is great news for buyers. As a recent article from Bankrate says:

“The rate cool-off somewhat eases the housing affordability squeeze.”

And according to Edward Seiler, AVP of Housing Economics and Executive Director of the Research Institute for Housing America at the Mortgage Bankers Association (MBA):

“MBA expects that affordability conditions will continue to improve as mortgage rates decline . . .”

Here’s a bit more context on how this could help with your plans to buy a home.

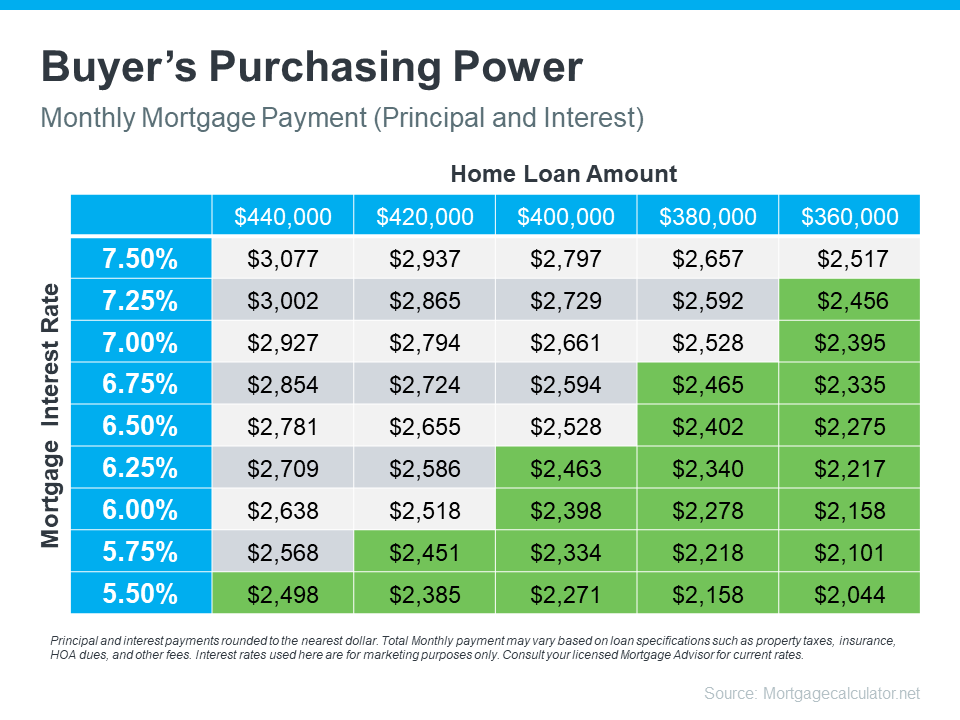

How Mortgage Rates Affect Your Search for a Home

Understanding the connection between mortgage rates and your monthly home payment is crucial for your plans to become a homeowner. The chart below illustrates how your ability to afford a home changes when mortgage rates shift. Imagine your budget allows for a monthly payment between $2,400 and $2,500. The green part in the chart shows payments in that range or lower (see chart below):

As you can see, even small changes in rates can affect your budget and the loan amount you can afford.

Get Help from Reliable Experts To Understand Your Budget and Plan Ahead

When you're looking to buy a home, it's important to get guidance from a local real estate agent and a trusted lender. They can help you explore different mortgage options, understand what makes mortgage rates go up or down, and how those changes impact you.

By looking at the numbers and the latest data together, then adjusting your strategy based on today's rates, you'll be better prepared and ready to buy a home.

Bottom Line

If you’re looking to buy a home, you should know the recent downward trend in mortgage rates is good news for your move. Let’s connect and plan your next steps.

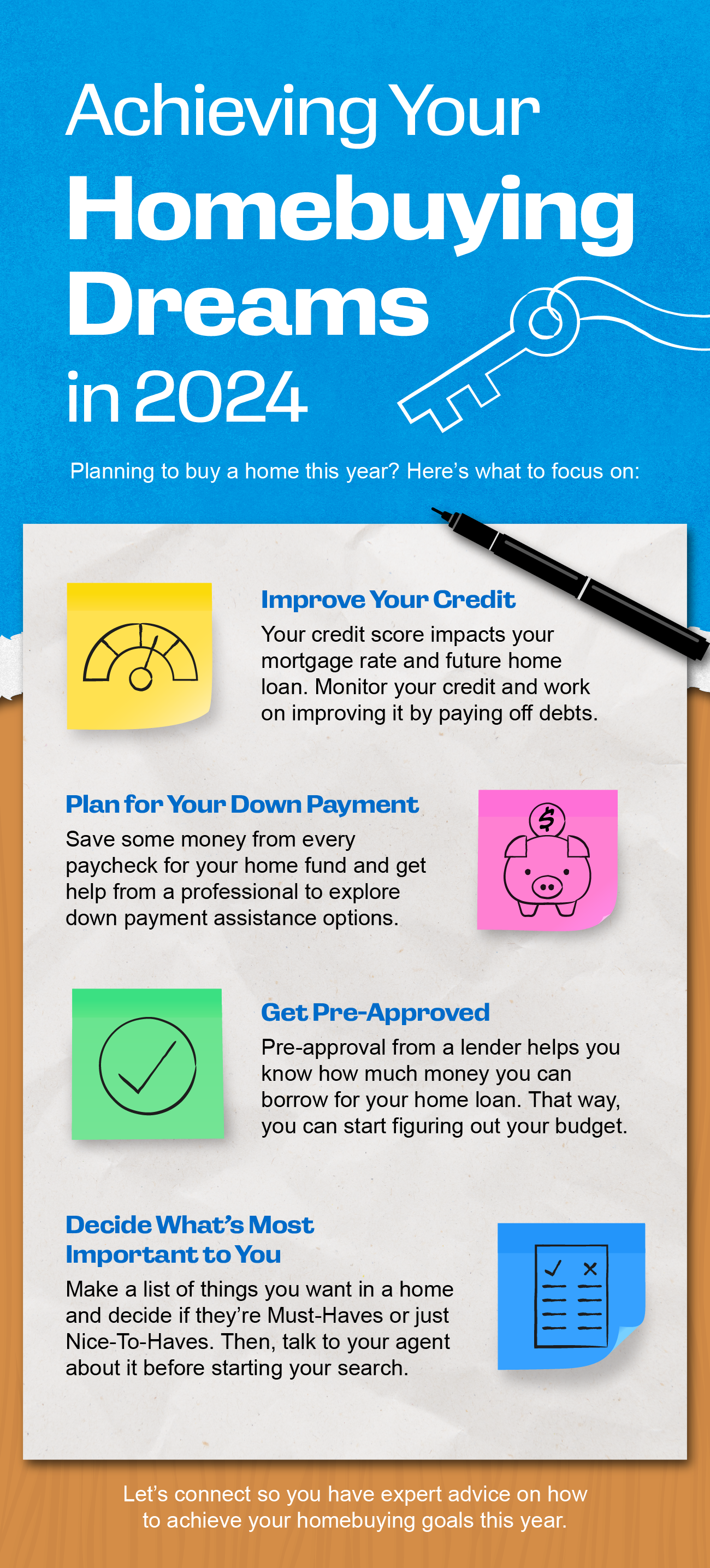

Achieving Your Homebuying Dreams in 2024 [INFOGRAPHIC]

Some Highlights

- Planning to buy a home in 2024? Here’s what to focus on.

- Improve your credit score, plan for your down payment, get pre-approved, and decide what’s most important to you.

- Let’s connect so you have expert advice on how to achieve your homebuying goals this year.

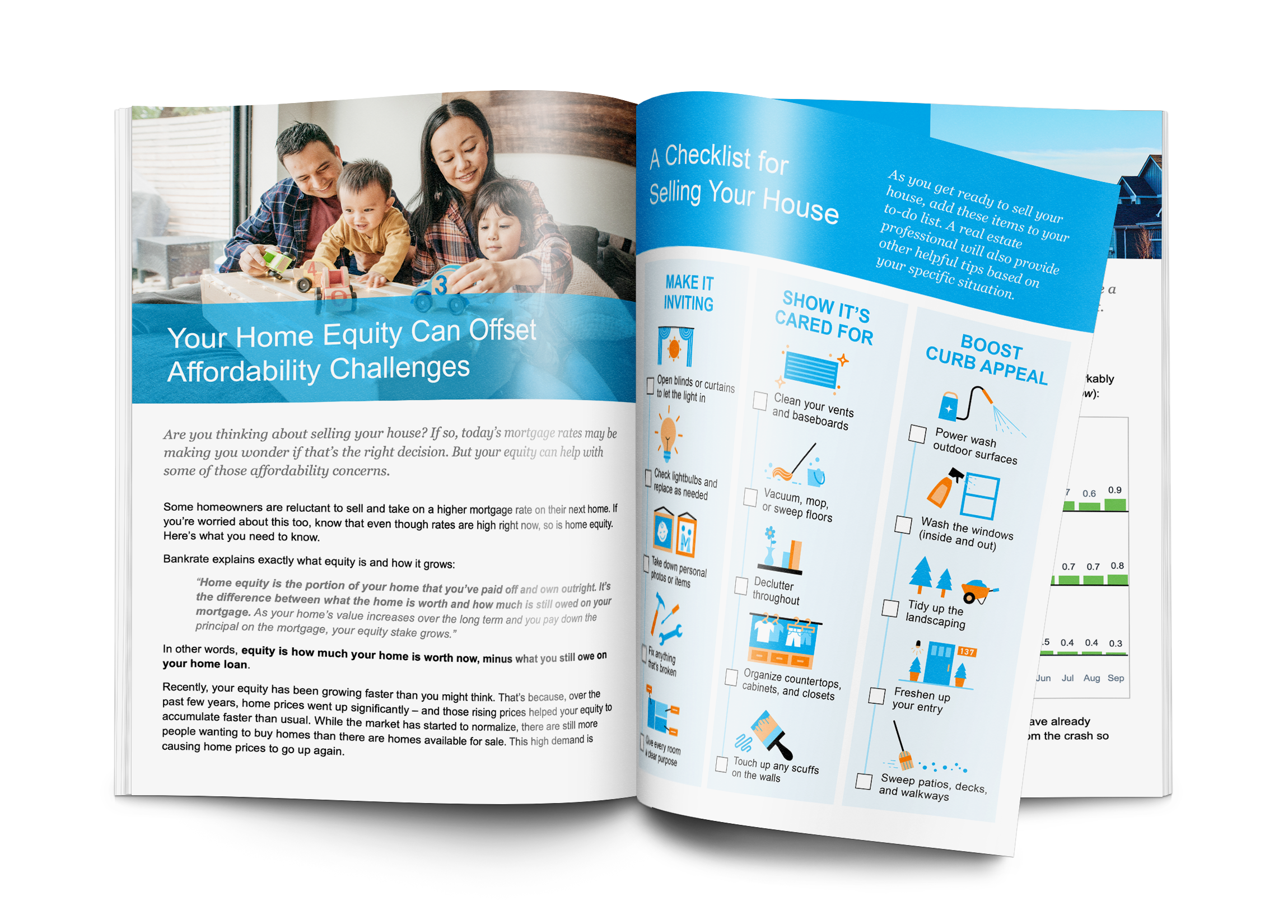

Things To Consider If Your House Didn’t Sell

If your listing has expired and your house didn’t sell, it's completely normal to feel a mix of frustration and disappointment. Understandably, you're probably wondering what may have gone wrong. Here are three questions to think about as you figure out what to do next.

Did You Limit Access to Your House?

One of the biggest mistakes you can make when selling your house is restricting the days and times when potential buyers can tour it. Being flexible with your schedule is important, even though it might feel a bit stressful to drop everything and leave when buyers want to see it. After all, minimal access means minimal exposure to buyers. ShowingTime advises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

Sometimes, the most

If buying or selling a home is your goal for 2024, it’s important to understand today’s housing market, know your why, and work with industry experts to bring your homeownership vision for the new year into focus. Over the last year, the economy had a big impact on the housing market, and likely on your wallet too. That’s why it’s critical to have a clear picture of not just the market today, but also on what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at Realtor.com, explains: Here are a few things to think through as you define your goals for 2024. You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time. Use your why and your motivation as a guidepost in partnership with an expert advisor to make sure your move gives you a lasting sense of accomplishment. You know you want to move, but how would you describe your dream home? The number of homes for sale has grown recently, and that could mean more options to choose from when you buy. But overall housing supply is still lower than more normal years in the market, so you’ll have to work closely with a pro to find what you’re looking for. Just be sure to keep your budget in mind as you balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it will be to find a home that’s right for you. Getting clear on your budget and available

3 Keys To Hitting Your Homeownership Goals in 2024

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

1. Know Your Why

2. Figure Out What Your Next Home Needs To Look Like

3. Determine if You’re Ready To Buy

Designated Broker, Co-Owner, GRI, Realtor®

EVANS REALTY LLC

1302 S Washington Ave

Emmett, ID 83617

Direct: (208) 365-4495

Cell: (208) 861-9090

Fax: (208) 955-2693

EMAIL

![]()

EVANS REALTY LLC

Emmett, ID 83617

PH: (208) 365-4495

CELL: (208) 861-9090

FAX: (208) 955-2693

Press Ctrl + D to bookmark this page

![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Member Agents | Privacy Policy

Realtor Websites by Tour Real Estate Inc.