Helpful real estate information and tips

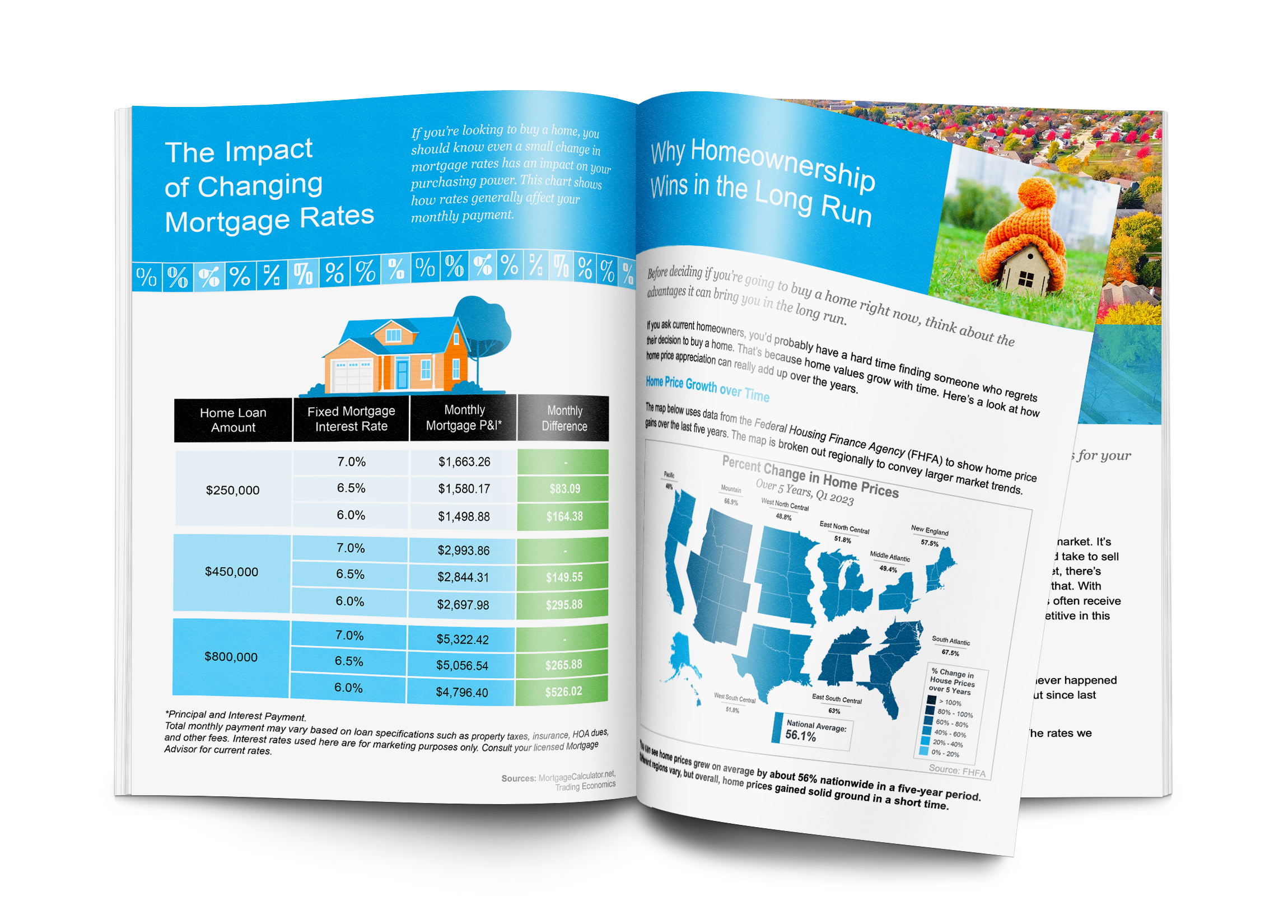

Home Prices Are Not Falling

During the fourth quarter of last year, some housing experts projected home prices were going to crash in 2023. The media ran with those forecasts and put out headlines calling for doom and gloom in the housing market. All of this negative news coverage made a lot of people have doubts about the strength of the residential real estate market.

If it made you question if you should delay your own plans to move, here’s what you really need to know.

Home Prices Never Crashed

Disregard what you saw in the headlines. The actual data shows home prices were remarkably resilient and performed far better than the media would have you believe (see graph below):

This graph uses reports from three trusted sources to clearly illustrate prices have already rebounded after experiencing only slight declines nationally. That’s a far cry from the crash so many articles called for.

The declines that did happen (shown in red), weren’t drastic but were short-lived. As Nicole Friedman, a reporter at the Wall Street Journal (WSJ), says:

“Home prices aren’t falling anymore. . . The surprisingly quick recovery suggests that the residential real-estate downturn is turning out to be shorter and shallower than many housing economists expected . . .”

Even though some media coverage made a big deal about home prices pulling back, the slight correction that happened is already in the rearview mirror. Basically, this data shows you home prices aren’t falling anymore – they’re actually going back up.

What’s Next for Home Prices?

The consensus from experts is that home price growth will continue in the years ahead and is returning to normal levels for the market. That means we’ll still see home prices appreciating, just at a slower pace than the last few years – and that’s a good thing.

Some news sources will see home price growth slowing and put out stories that make you think prices are falling again. The return of misleading headlines like those is already having an impact on how homebuyers are feeling again. You can see how this affects general opinion in the Consumer Confidence Survey from Fannie Mae (see graph below):

While the percentage of Americans who think prices will fall has been slowly declining this year, the latest Consumer Confidence data indicates that’s ticked back up recently (shown in red). This change is surprising especially since the home price data shows prices are going up, not down. It tells you the impact the media still has on public opinion.

Don’t fall for the negative headlines and become part of this statistic. Remember, data from a number of sources shows home prices aren’t falling anymore.

Bottom Line

Even though the media may make things sound doom and gloom, the data shows home prices aren’t falling anymore. So, don’t let the headlines scare you or delay your plans. Let's connect so you have a trusted resource to cut through the noise and tell you what’s really happening in our area.

Explaining Today’s Low Housing Supply [INFOGRAPHIC]

Some Highlights

- Wondering why the supply of homes for sale is limited today? There are a few factors at play.

- Lack of building over time, the mortgage rate lock-in effect, and people staying in their houses longer are three of the main reasons why supply is low.

- But real estate agents know exactly where to look and what to do to make your dream a reality. Let’s connect so you have an expert on your side to help you successfully navigate the market and find your next home.

Why Your House Didn’t Sell

If your listing expired and your house didn’t sell, you’re likely feeling a little frustrated. Not to mention, you're also probably wondering what went wrong. Here are three questions to think about as you figure out what to do next.

Did You Limit Access to Your House?

One of the biggest mistakes you can make when selling your house is restricting the days and times when potential buyers can tour it. Being flexible with your schedule is important when you're selling your house, even though it might feel a bit stressful to drop everything and leave when buyers want to see it. After all, minimal access means minimal exposure to buyers. ShowingTime advises:

“. . . do your best to be as flexible as possible when granting access to your house for showings.”

Sometimes, the most determined buyers might come from far away. Since they're traveling to see your house, they may not be able to change their plans easily if you only offer limited times for showings. So, try to make your house available as much as you can to accommodate them. It’s simple. If no one’s able to look at it, how’s it going to sell?

Did You Make Your House Stand Out?

When selling your house, the old saying matters: you never get a second chance to make a first impression. Putting in the work to make the exterior of your home look nice is just as important as how you stage it inside. Freshen up your landscaping to improve your home’s curb appeal so you can make an impact upfront. As an article from U.S. News says:

“After all, if people drive by, but aren’t interested enough to walk through the front door, you’ll never sell your house.”

But don’t let that impact stop at the front door. By removing personal items and reducing clutter inside, you give buyers more freedom to picture themselves in the home. Additionally, a new coat of paint or cleaning the floors can go a long way to freshening up a room.

Did You Price Your House Compellingly?

Setting the right price is extremely important when you're selling your house. Even though it might feel tempting to push the price higher to maximize your profit, overpricing can scare away buyers and make it hard to sell quickly. Business Insider notes:

“. . . the biggest mistake sellers make is overpricing their home.”

If your house is priced higher than others like it, it could make buyers lose interest. Pay attention to the feedback people give your agent during open houses and showings. If lots of people are saying the same thing, it might be a good idea to think about lowering the price.

For all these insights and more, rely on a trusted real estate agent. A great agent will offer expert advice on relisting your house with effective strategies to get it sold.

Bottom Line

It’s natural to feel disappointed when your listing has expired and your house didn’t sell. Let’s connect to figure out what happened and what to reconsider or change if you want to get your house back on the market.

Why Today’s Housing Inventory Shows a Crash Isn’t on the Horizon

You might remember the housing crash in 2008, even if you didn't own a home at the time. If you’re worried there’s going to be a repeat of what happened back then, there's good news – the housing market now is different from 2008.

One important reason is there aren't enough homes for sale. That means there’s an undersupply, not an oversupply like the last time. For the market to crash, there would have to be too many houses for sale, but the data doesn't show that happening.

Housing supply comes from three main sources:

- Homeowners deciding to sell their houses

- Newly built homes

- Distressed properties (foreclosures or short sales)

Here’s a closer look at today's housing inventory to understand why this isn’t like 2008.

Homeowners Deciding To Sell Their Houses

Although housing supply did grow compared to last year, it’s still low. The current months’ supply is below the norm. The graph below shows this more clearly. If you look at the latest data (shown in green), compared to 2008 (shown in red), there’s only about a third of that available inventory today.

So, what does this mean? There just aren't enough homes available to make home values drop. To have a repeat of 2008, there’d need to be a lot more people selling their houses with very few buyers, and that's not happening right now.

Newly Built Homes

People are also talking a lot about what's going on with newly built houses these days, and that might make you wonder if homebuilders are overdoing it. The graph below shows the number of new houses built over the last 52 years:

The 14 years of underbuilding (shown in red) is a big part of the reason why inventory is so low today. Basically, builders haven’t been building enough homes for years now and that’s created a significant deficit in supply.

While the final blue bar on the graph shows that’s ramping up and is on pace to hit the long-term average again, it won’t suddenly create an oversupply. That’s because there’s too much of a gap to make up. Plus, builders are being intentional about not overbuilding homes like they did during the bubble.

Distressed Properties (Foreclosures and Short Sales)

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back during the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to get a home loan they couldn’t truly afford.

Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from the Federal Reserve to show how things have changed since the housing crash:

This graph illustrates, as lending standards got tighter and buyers were more qualified, the number of foreclosures started to go down. And in 2020 and 2021, the combination of a moratorium on foreclosures and the forbearance program helped prevent a repeat of the wave of foreclosures we saw back around 2008.

The forbearance program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. And data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

What This Means for You

Inventory levels aren’t anywhere near where they’d need to be for prices to drop significantly and the housing market to crash. According to Bankrate, that isn’t going to change anytime soon, especially considering buyer demand is still strong:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

Bottom Line

The market doesn’t have enough available homes for a repeat of the 2008 housing crisis – and there’s nothing that suggests that will change anytime soon. That’s why housing inventory tells us there’s no crash on the horizon.

The Return of Normal Seasonality for Home Price Appreciation

If you’re thinking of making a move, one of the biggest questions you have right now is probably: what’s happening with home prices? Despite what you may be hearing in the news, nationally, home prices aren’t falling. It’s just that price growth is beginning to normalize. Here’s the context you need to really understand that trend.

In the housing market, there are predictable ebbs and flows that happen each year. It’s called seasonality. Spring is the peak homebuying season when the market is most active. That activity is typically still strong in the summer but begins to wane as the cooler months approach. Home prices follow along with seasonality because prices appreciate most when something is in high demand.

That’s why there’s a reliable long-term home price trend. The graph below uses data from Case-Shiller to show typical monthly home price movement from 1973 through 2022 (not adjusted, so you can see the seasonality):

As the data shows, at the beginning of the year, home prices grow, but not as much as they do in the spring and summer markets. That’s because the market is less active in January and February since fewer people move in the cooler months. As the market transitions into the peak homebuying season in the spring, activity ramps up, and home prices go up a lot more in response. Then, as fall and winter approach, activity eases again. Price growth slows, but still typically appreciates.

After several unusual ‘unicorn’ years, today’s higher mortgage rates helped usher in the first signs of the return of seasonality. As Selma Hepp, Chief Economist at CoreLogic, explains:

“High mortgage rates have slowed additional price surges, with monthly increases returning to regular seasonal averages. In other words, home prices are still growing but are in line with historic seasonal expectations.”

Why This Is So Important to Understand

In the coming months, you’re going to see the media talk more about home prices. In their coverage, you’ll likely see industry terms like these:

- Appreciation: when prices increase.

- Deceleration of appreciation: when prices continue to appreciate, but at a slower or more moderate pace.

- Depreciation: when prices decrease.

Don’t let the terminology confuse you or let any misleading headlines cause any unnecessary fear. The rapid pace of home price growth the market saw in recent years was unsustainable. It had to slow down at some point and that’s what we’re starting to see – deceleration of appreciation, not depreciation.

Remember, it’s normal to see home price growth slow down as the year goes on. And that definitely doesn’t mean home prices are falling. They’re just rising at a more moderate pace.

Bottom Line

While the headlines are generating fear and confusion on what’s happening with home prices, the truth is simple. Home price appreciation is returning to normal seasonality. If you have questions about what’s happening with prices in our local area, let’s connect.

Designated Broker, Co-Owner, GRI, Realtor®

EVANS REALTY LLC

1302 S Washington Ave

Emmett, ID 83617

Direct: (208) 365-4495

Cell: (208) 861-9090

Fax: (208) 955-2693

EVANS REALTY LLC

Emmett, ID 83617

PH: (208) 365-4495

CELL: (208) 861-9090

FAX: (208) 955-2693

Press Ctrl + D to bookmark this page

Web Accessibility Help Visually Impaired

Physical Difficulty

Audio Impaired

|

|

Member Agents | Privacy Policy

Realtor Websites by Tour Real Estate Inc.