Helpful real estate information and tips

Experts Project Home Prices Will Increase in 2024

Even though home prices are going up nationally, some people are still worried they might come down. In fact, a recent survey from Fannie Mae found that 24% of people think home prices will actually decline over the next 12 months. That means almost one out of every four people are dealing with that fear, and you might be, too.

To help ease that concern, here's what experts forecast will happen with prices this year.

Experts Project a Modest Increase

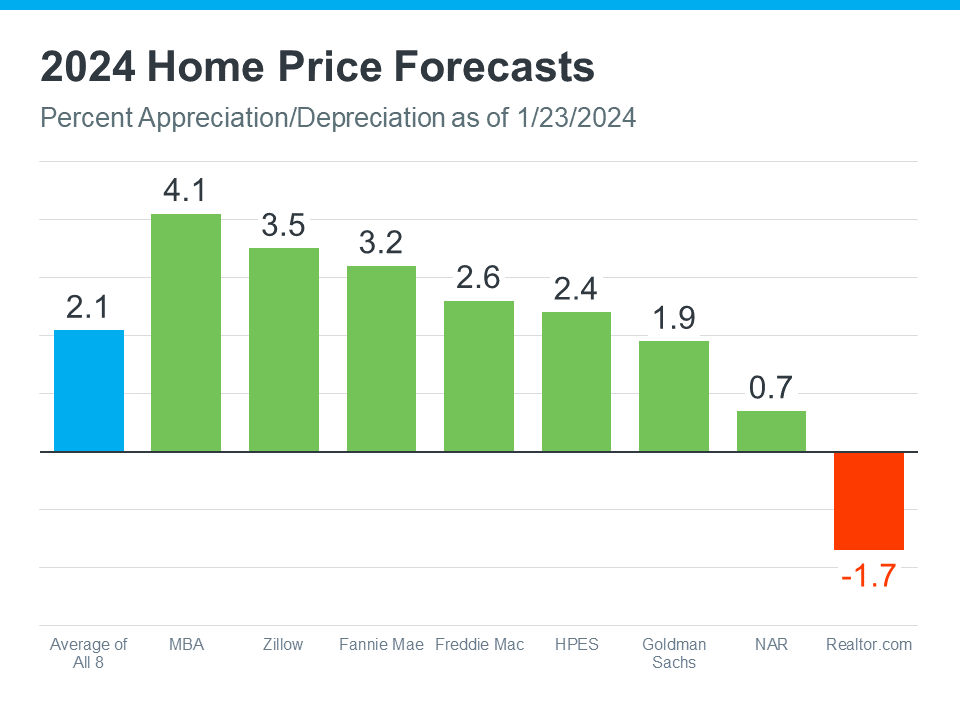

Check out the latest home price forecasts from eight different sources (see graph below):

The blue bar on the left means, on average, experts think home prices will go up over 2% by the end of this year – not down.

Prices aren’t likely to depreciate in 2024 because inventory is still tight and lower mortgage rates are leading to strong buyer demand. Those two factors will keep pushing prices up as the year goes on. As Selma Hepp, Chief Economist at CoreLogic, explains:

“With mortgage rates dropping, demand for homes in early 2024 is likely to be strong and will again put pressure on prices, similar to trends observed in early 2023 . . . Most markets will continue to reach new home price highs over the course of 2024.”

What Does This Mean for You?

Experts are saying home prices will go up this year, and that's good news if you're thinking about buying a home. When you become a homeowner, you want the value of your house to go up. That appreciation is what builds equity and makes homeownership such a good investment over time.

Beyond that, expected home price appreciation also means if you’re ready, willing, and able to buy, waiting just means it will cost more later.

Bottom Line

If you're worried home prices will come down, don’t be. Many experts believe they’ll actually go up this year. If you have questions or worries about what’s happening with prices in our area, let’s connect.

3 Must-Do’s When Selling Your House in 2024

If one of the goals on your list is selling your house and making a move this year, you’re likely juggling a mix of excitement about what’s ahead and feeling a little sentimental about your current home.

A great way to balance those emotions and make sure you’re confident in your decision is to keep these three best practices in mind when you’re ready to sell.

1. Price Your Home Right

The housing market shifted in 2023 as mortgage rates rose and home price appreciation started to normalize once again. As a seller, you still need to recognize how important it is to price your house appropriately based on where the market is today. Hannah Jones, Economic Research Analyst for Realtor.com, explains:

“Sellers need to become familiar with their local market and work closely with a local agent to make sure their listing is attractive to buyers. Buyers feeling the pressure of affordability are likely to be pickier, so a well-priced, well-maintained home is the ticket to drumming up big demand.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be, so your house moves quickly and for top dollar.

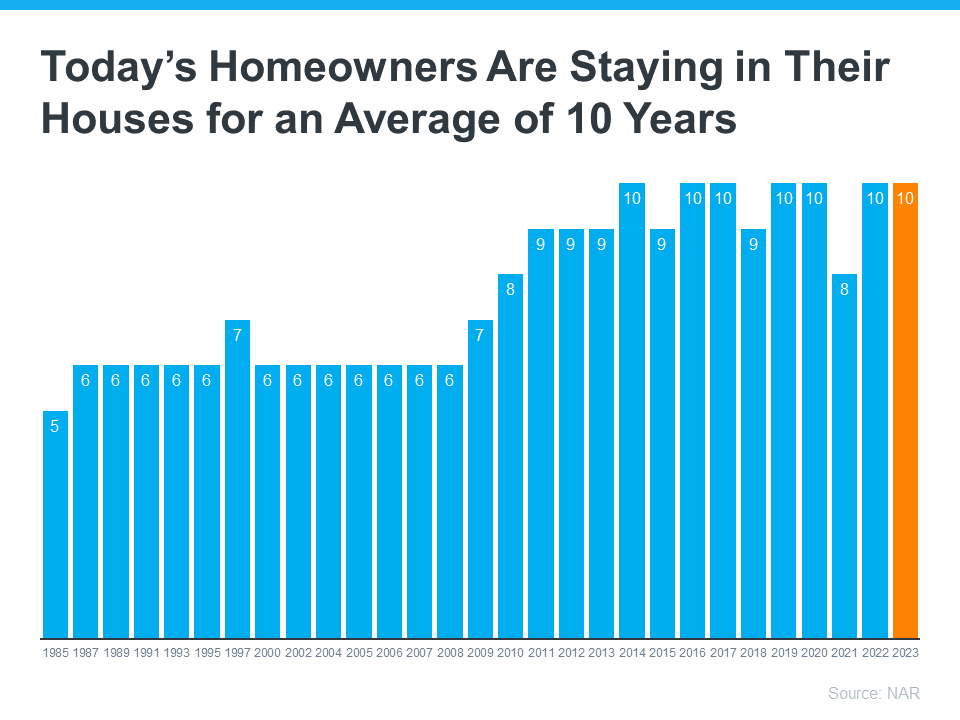

2. Keep Your Emotions in Check

Today, homeowners are staying in their houses longer than they used to. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 6 to 10 years (see graph below):

This is much more than what used to be the norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even tougher to separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations and the best pricing strategy along the way. Trust the professionals who have your best interests in mind.

3. Stage Your Home Properly

While you may love your decor and how you’ve customized your house over the years, not all buyers will feel the same way about your vibe. That’s why it’s so important to make sure you focus on your home’s first impression, so it appeals to as many buyers as possible.

Buyers want to be able to picture themselves in the home. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. As Jessica Lautz, Deputy Chief Economist and Vice President of Research at NAR, says:

“Buyers want to easily envision themselves within a new home and home staging is a way to showcase the property in its best light.”

A real estate professional can help you with expertise on getting your house ready to sell.

Bottom Line

If you’re considering selling your house, let’s connect so you have help navigating the process while prioritizing these must-do’s.

Why You May Want To Seriously Consider a Newly Built Home

Are you putting off your plans to sell because you’re worried you won’t be able to find a home you like when you move? If so, it may be time to consider a newly built home and the benefits that come with one. Here’s why.

Near-Record Percentage of New Home Inventory

Newly built homes are becoming an increasingly significant part of today’s housing inventory. According to the most recent report from the National Association of Home Builders (NAHB):

“Newly built homes available for sale accounted for 31% of total homes available for sale in November, compared to an approximate 12% historical average.”

That means the percentage of the total homes available to buy that are newly built is well over two times higher than the norm. And even more new homes are on the way.

Recent data from the Census shows there’s been an uptick in both housing starts (where builders break ground on more new homes) and housing completions (homes where construction just wrapped).

And while some people may worry builders are building too many homes, that isn’t a concern – if anything, the recent increase is really good news. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Even more home building will be needed with the housing shortage persisting in most markets . . . Another 30% rise in home construction can easily be absorbed in the marketplace . . .”

How This Helps You

Since the supply of existing homes for sale is still low right now, the increase of new-home construction can be a game changer because it gives you more options for your search.

Picture yourself in a home that’s new from the ground up: new appliances, fresh paint, fewer maintenance needs because everything is new, and so much more. Doesn’t that sound nice?

And it may be more within reach than you ever imagined. In addition, some builders are offering things like mortgage rate buy-downs for homebuyers right now. This can help offset today’s affordability challenges while also getting you into your dream home. In a recent article, Patrick Duffy, Senior Real Estate Economist at U.S. News, explains:

“Builders have been using mortgage interest rate buydowns for many years as a sales incentive whenever interest rates are relatively high, . . .Today more builders are offering rate buydowns for the entirety of the loan, allowing buyers to finance more home for the same payment amount.”

Just remember, the process of buying from a builder is different from buying from a home seller, so it’s important to partner with a trusted real estate agent who knows the local market. They’ll be your go-to resource for coordinating with the builder, reviewing contracts, and more.

Bottom Line

If you’re trying to sell so you can make a move but you’re having a hard time finding a home you like, let’s connect. That way you have a local expert to help you explore all of your options, including the newly built homes in our area.

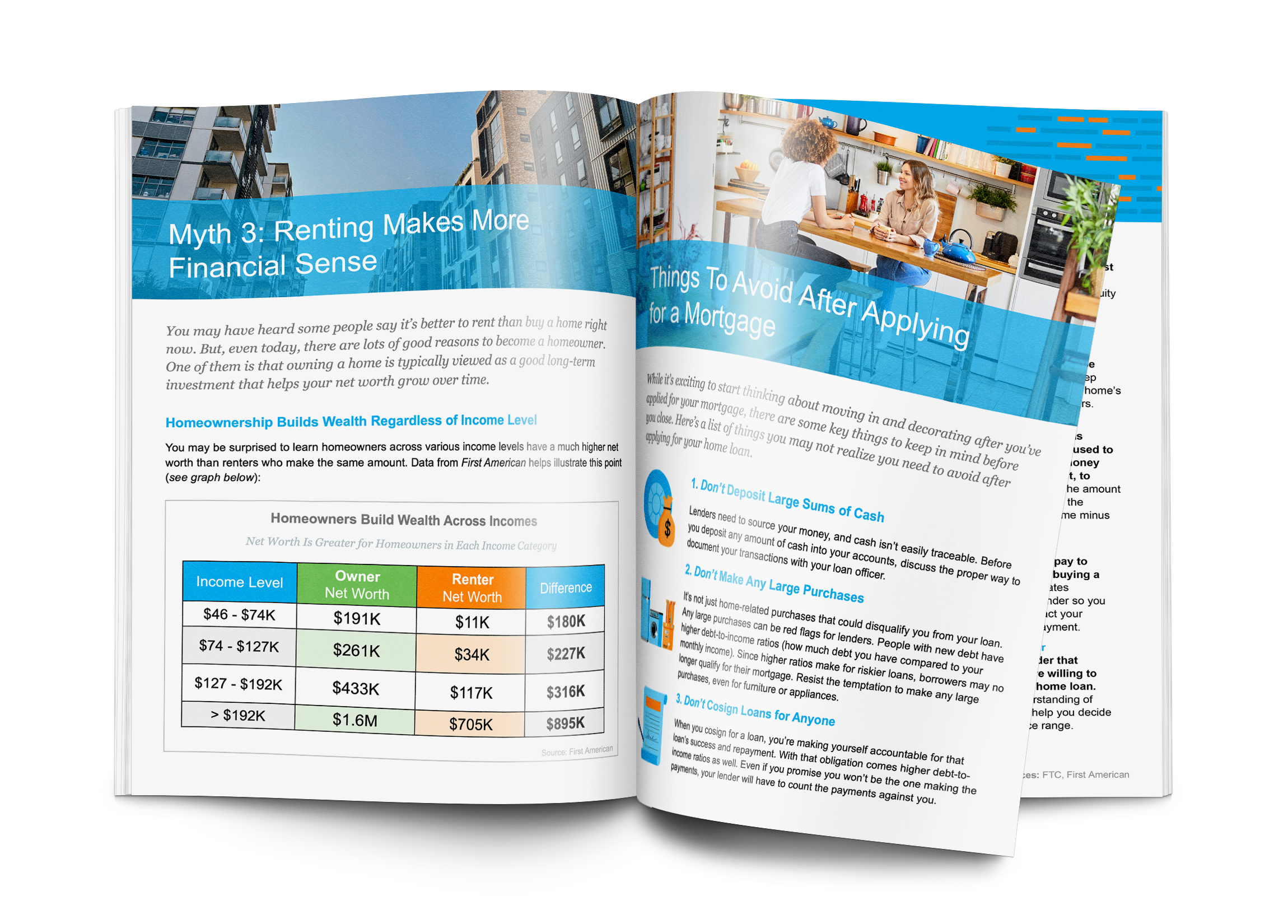

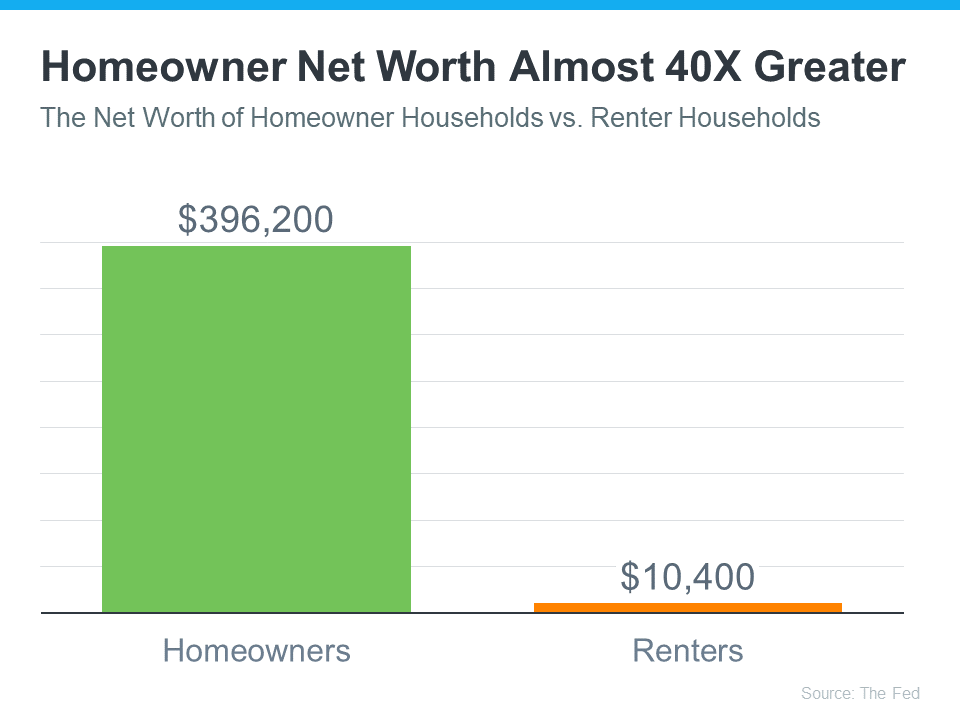

The Dramatic Impact of Homeownership on Net Worth

If you're trying to decide whether to rent or buy a home this year, here's a powerful insight that could give you the clarity and confidence you need to make your decision.

Every three years, the Federal Reserve releases the Survey of Consumer Finances (SCF), which compares net worth for homeowners and renters. The latest report shows the average homeowner’s net worth is almost 40X greater than a renter’s (see graph below):

One reason a wealth gap exists between renters and homeowners is because when you’re a homeowner, your equity grows as your home appreciates in value and you make your mortgage payment each month. When you own a home, your monthly mortgage payment acts like a form of forced savings, which eventually pays off when you decide to sell. As a renter, you’ll never see a financial return on the money you pay out in rent every month. Ksenia Potapov, Economist at First American, explains it like this:

“Renters don’t capture the wealth generated by house price appreciation, nor do they benefit from the equity gains generated by monthly mortgage payments . . .”

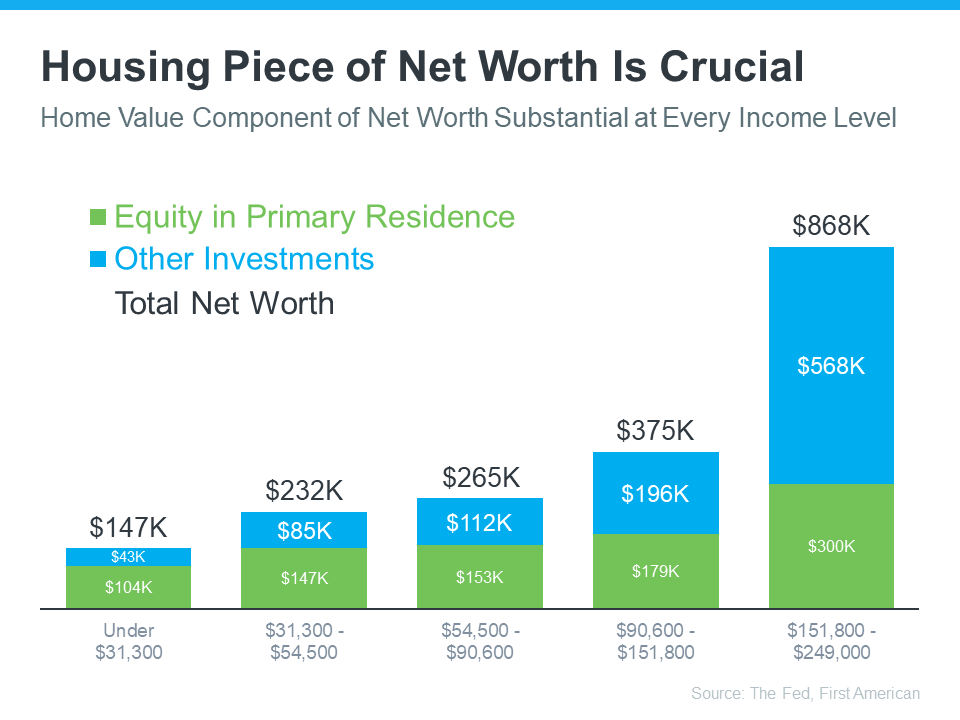

The Largest Part of Most Homeowner Net Worth Is Their Equity

Home equity does more to build the average household’s wealth than anything else. According to data from First American and the Federal Reserve, this holds true across different income levels (see graph below):

The green segment in each bar represents how much of a homeowner's net worth comes from their home equity. Based on this data, it's clear no matter what your income level is, owning a home can really boost your wealth. Nicole Bachaud, Senior Economist at Zillow, shares:

“The biggest asset most people are ever going to own is a home. Homeownership is really that financial key that helps unlock stability and wealth preservation across generations.”

If you’re ready to start building your net worth, the current real estate market offers several opportunities you should consider. For example, with mortgage rates trending lower lately, your purchasing power may be higher now than it has been in months. And, with more inventory coming to the market, there are more options for you to consider. A local real estate agent can walk you through the opportunities you have today and guide you through the process of finding your ideal home.

Bottom Line

If you're unsure about whether to rent or buy a home, keep in mind that owning a home can increase your overall wealth in the long run, no matter your income. To discover more about this and the many other benefits of homeownership, let’s connect.

Avoid These Common Mistakes After Applying for a Mortgage

If you’re getting ready to buy a home, it’s exciting to jump a few steps ahead and think about moving in and making it your own. But before you get too far down the emotional path, there are some key things to keep in mind after you apply for your mortgage and before you close. Here’s a list of things to remember when you apply for your home loan.

Don’t Deposit Large Sums of Cash

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any cash into your accounts, discuss the proper way to document your transactions with your loan officer.

Don’t Make Any Large Purchases

It’s not just home-related purchases that could disqualify you from your loan. Any large purchases can be red flags for lenders. People with new debt have higher debt-to-income ratios (how much debt you have compared to your monthly income). Since higher ratios make for riskier loans, borrowers may no longer qualify for their mortgage. Resist the temptation to make any large purchases, even for furniture or appliances.

Don’t Cosign Loans for Anyone

When you cosign for a loan, you’re making yourself accountable for that loan’s success and repayment. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count them against you.

Don’t Switch Bank Accounts

Lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

Don’t Apply for New Credit

It doesn’t matter whether it’s a new credit card or a new car. When your credit report is run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), it will have an impact on your FICO® score. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

Don’t Close Any Accounts

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those parts of your score.

Do Discuss Changes with Your Lender

Be upfront about any changes that occur or you’re expecting to occur when talking with your lender. Blips in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. Ultimately, it’s best to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

Bottom Line

You want your home purchase to go as smoothly as possible. Remember, before you make any large purchases, move your money around, or make major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

Designated Broker, Co-Owner, GRI, Realtor®

EVANS REALTY LLC

1302 S Washington Ave

Emmett, ID 83617

Direct: (208) 365-4495

Cell: (208) 861-9090

Fax: (208) 955-2693

EVANS REALTY LLC

Emmett, ID 83617

PH: (208) 365-4495

CELL: (208) 861-9090

FAX: (208) 955-2693

Press Ctrl + D to bookmark this page

Web Accessibility Help Visually Impaired

Physical Difficulty

Audio Impaired

|

|

Member Agents | Privacy Policy

Realtor Websites by Tour Real Estate Inc.